Congress is considering an extension of extra help for people buying their own health coverage on the Affordable Care Act Marketplaces. These temporary subsidies, passed as part of the American Rescue Plan Act (ARPA), increased the amount of financial help available to those already eligible; the ARPA also newly expanded subsidies to middle-income people, many of whom were previously priced out of coverage.

See how 2022 premium payments would increase without the ARPA COVID-19 relief law’s enhanced tax credits. Click the images below to access two versions of the calculator.

There are reports Congress is considering a temporary extension of the subsidies for two years. If these subsidies expire, either at the end of this year or after a temporary renewal, premium payments will rise. Here’s what to know:

The Big Picture: How Much Higher Would Premium Payments be Without ARPA?

If Congress extends the temporary subsidies, premium payments in 2023 will hold mostly flat for Marketplace enrollees, since the premium tax credits shelter enrollees from increases in the underlying premium. However, if these extra subsidies expire, out-of-pocket premium payments will rise across the board next year for virtually all 13 million subsidized enrollees. In the 33 states using HealthCare.gov, premium payments in 2022 would have been 53% higher on average if not for the ARPA extra subsidies. The same is true in the states operating their own exchanges.

Exactly how much of a premium increase enrollees would see if these subsidies expire depends on the enrollee’s income, age, and the premiums where they live.

For example, using our subsidy calculator, you can see that with the ARPA a 40-year-old couple making $25,000 per year currently pays $0 for a silver plan premium with significantly lowered out-of-pocket deductible costs. Using a new version of our subsidy calculator that shows what premium payments in each zip code would have been if the ARPA had not passed, you can see that same couple would have paid $76 per month (or $915 over the course of 2022) without the ARPA. If Congress extends the ARPA subsidies, though, this low-income couple would save $915.

Here’s another example using the new calculator: If the ARPA hadn’t passed, a 60-year-old couple with an income of $70,000 would have had to pay $1,859 per month (or $22,307 over the course of 2022) for a full-price silver plan. Now, compare this to our 2022 calculator that shows what they currently pay with the ARPA: The same couple currently pays $496 per month (or $5,950 over the course of the year). Instead of being expected to pay about 32% of their income on insurance, which would likely be unaffordable, the couple is paying 8.5% of their income with the ARPA. So, if Congress extends the ARPA subsidies, this older middle-income couple will save over $16,000.

The Double Whammy: How 2023 Premium Increases and Subsidy Expiration Would Affect Some Enrollees

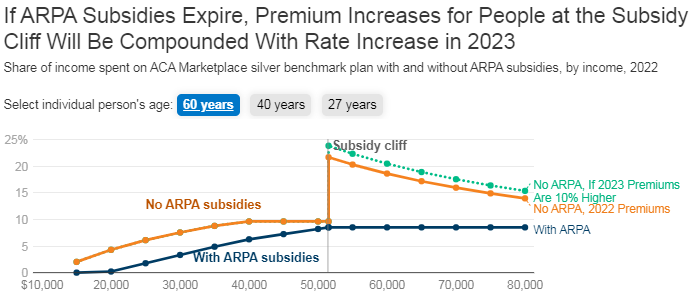

The renewal of these subsidies would also prevent some enrollees from experiencing two kinds of premium increases at once. If Congress does not extend these subsidies, the subsidy cliff would return, meaning people with incomes over four times poverty (or about $51,520 for a single person) would lose subsidy eligibility altogether. So, without the ARPA subsidies, these enrollees would not only pay the increase due to the loss of subsidies, but also any increase in the underlying premium.

Our early look at 2023 premiums shows premiums rising about 10%, with most rate increases falling between about 5% and 14%. This is more than in past years, in part due to inflation and rebounding utilization. These rates are still proposed and will not be finalized until next month.

The figure below shows a hypothetical subsidy cliff if premiums do indeed rise by 10%. For example, a 60-year-old making just above four times poverty ($51,521) in 2022 pays 8.5% of their income on a silver plan under ARPA, but would have paid 22% of their income in 2022 without the ARPA on average across the U.S. If premiums rise 10%, they would pay 24% of their income in 2023.

In the states where premiums are currently highest, people losing subsidies would see the steepest increases without the ARPA subsidies. For example, a 60-year-old making just above four times poverty ($51,521) in 2022 would pay more than a third of their income on a silver plan without the ARPA in West Virginia and Wyoming; and in New Hampshire, the person would have paid 15% of their income without ARPA.

The Ticking Clock: Why the Timing Matters

Insurers are now in the process of setting 2023 premiums and some are already factoring in an additional premium increase because they expect ARPA subsidies to expire.

The National Association of Insurance Commissioners (NAIC) wrote to Congress asking to extend these subsidies by July to provide greater certainty as insurers set premiums for next year. Premiums for 2023 are locked in by this August, so if Congress does not act before its August recess, whatever assumptions insurers make about the future of ARPA subsidies will be factored in to their 2023 premiums.

States and the federal government, which operates HealthCare.gov, will need to reprogram their enrollment websites and train consumer support staff on policy changes months ahead of open enrollment this fall. If Congress ultimately extends the enhanced ACA subsidies but does not give state and federal exchange administrators enough lead time to make changes to enrollment websites, people shopping for coverage may get incorrect information or may temporarily lose access to subsidies, causing some to drop coverage.

The End of the Public Health Emergency: How Enhanced Marketplace Subsidies Could Mitigate Coverage Loss

The end of the public health emergency and, with it, the requirement for continuous enrollment in Medicaid is expected to lead to significant coverage losses. So far, the number of uninsured people has not grown during the pandemic and resulting economic crisis. However, ironically, we could see a jump in the uninsured rate as the public health emergency ends if people disenrolled from Medicaid do not find alternative coverage.

Enhanced Marketplace subsidies could act as a bridge between Medicaid and the ACA Marketplaces when the public health emergency ends. If enhanced Marketplace subsidies are still in place when the Medicaid maintenance of eligibility (MOE) ends, many people disenrolled from Medicaid could find similarly low-cost coverage on the ACA Marketplaces. If they are eligible for Marketplace subsidies, people losing Medicaid coverage may find Marketplace plans that, like Medicaid, have zero (or near-zero) monthly premium requirement, assuming the enhanced assistance is extended.

The Costs: What This Means for the Federal Budget

The Congressional Budget Office (CBO) expects the enhanced subsidies to cost about $248 billion over the course of ten years if extended permanently. A large part of the estimated cost is due to the CBO’s expectation that 4.8 million more people would enroll in the ACA Marketplaces than would if the enhanced subsidies are not extended. The actual cost will depend on how many people enroll and how much premiums rise over the coming years. Congress could lower the total cost by extending subsidies temporarily, for example by two or three years, but the annual cost would likely stay about the same.

Conclusion

Health sector inflation, rising utilization, and other factors may cause 2023 premiums to rise by more than in past years. However, as we’ve written before, Congress’s action or inaction on ARPA subsidies will have an even greater influence over how much subsidized ACA Marketplace enrollees pay out-of-pocket for their premiums than will market-driven factors that affect the underlying premium.

Whether subsidies expire at the end of this year or in two or three years, their expiration would result in the steepest increase in out-of-pocket premium payments most enrollees in this market have seen.

"about" - Google News

July 22, 2022 at 11:42PM

https://ift.tt/Aro93g1

Five Things to Know about the Possible Renewal of Extra Affordable Care Act Subsidies - Kaiser Family Foundation

"about" - Google News

https://ift.tt/xd7jWQ9

Bagikan Berita Ini

0 Response to "Five Things to Know about the Possible Renewal of Extra Affordable Care Act Subsidies - Kaiser Family Foundation"

Post a Comment